AutoZone: Annual Update

There’s a small subset of businesses that thrive during recessions. Good in the best of times, they become extraordinary during the tough times. AutoZone is one of these businesses.

As proof, consider that AutoZone did not lay off or furlough a single employee during the pandemic. Lots of businesses talk about treating their employees right. AutoZone walks the walk.

Of course, it helped that AutoZone’s sales exploded.

Source: Author, Data from 2020 10-K

The stability of these quarterly numbers belie what actually happened to AutoZone. The pandemic affected the company much more severely and violently than the quarterly numbers let on. Over a four-week period in April, sales plummeted over 20% as shutdowns and reduced hours took their toll. Then, as stimulus checks arrived, sales rebounded as forcefully as they fall. The late spring rush made up for the early-spring lockdowns, resulting in a wash for fiscal Q3. But the rush kept coming long after the government stimulus ended, resulting in a record 22% sales increase in Q4.

This sales spike was the result of a confluence of factors:

AutoZone’s core customers disposable income rose due to:

Government stimulus checks and increased unemployment benefits, and;

Less income spent on entertainment such as vacations, restaurants, and trips to the movie theatre as a result of the pandemic.

Less time traveling, eating out, and commuting allowed more time to work on cars. Some of these projects were discretionary upgrades customers had planned to do when they found the time. Others were catch-up maintenance projects.

The fourth-quarter surge brought the fiscal year’s total sales growth to 7%. This drove operating leverage that brought the company’s return on invested capital to 38%. Not bad for an inventory-heavy retailer during a pandemic!

Of course, the million-dollar question is, will the good times continue to roll? Or will sales revert back to their pre-pandemic rate?

Historically, AutoZone’s sales growth has been the strongest coming out of recessions. While history doesn’t repeat, it often rhymes, and we think history is instructive to study here. CEO Bill Rhodes explained on the most recent quarterly call:

“Last quarter, I reminded folks, the strongest periods we have experienced of outside sales growth over the last three decades have been the early 1990s, ‘01, ‘02, ‘09, ‘10 and ‘11, all coming out of recessionary periods. This is why we remain optimistic on the industry this upcoming year.

Interestingly, after each of those outsized sales growth periods, they have never been followed by equivalent declines in the years that follow. We believe consumer behaviors changed during these recessionary periods, allowing us to showcase our skills and capabilities to new customers, and we retain many of those customers in the years that follow.”

O’Reilly, AutoZone’s closest competitor, reported that sales through September “remained strong and are trending slightly below our third-quarter exit rate in the low double-digit range.” This suggests that, at least so far, AutoZone has probably kept a lot of the new customers it acquired.

We previously wrote that AutoZone’s comparable sales are closely related to miles driven and average vehicle age. Miles driven tend to increase most years, but not this year. They are down 11% from their February 2020 peak.

Source: St. Louis Federal Reserve

Nevertheless, AutoZone’s sales exploded. The reason for the dichotomy is that AutoZone’s core customers are blue-collar workers who are still commuting to work. White-collar knowledge workers are responsible for the overall decline in miles driven, but they don’t frequent AutoZone. Management thinks that miles driven by AutoZone’s core customers are stable.

Average vehicle age tends to increase during recessions because people hold onto older cars longer to delay a big cash outlay. Used car prices are now at all-time highs, suggesting that this is almost surely playing out again.

Besides AutoZone’s strong historical record coming out of recessions, we are optimistic because AutoZone’s competitive position has strengthened during the pandemic.

From what we’ve seen, the pandemic has not created any new trends. Rather, it’s accelerated the trends that were already in place. Some, like remote work, were nascent (but visible). Others, like AutoZone taking share from Mom & Pop auto parts stores, were well established.

Many Mom & Pop stores didn’t have the resources to weather lockdown and couldn’t keep up with the torrid pace of demand when they reopened. AutoZone, with greater resources, was able to keep up and gain market share.

AutoZone’s commercial business is an especially bright spot. Today this is a relatively minor part of AutoZone’s overall business, but it has big potential. AutoZone estimates its commercial market share today is only 5%. Commercial sales are largely incremental to AutoZone’s DIY business because they leverage existing infrastructure, giving them particularly attractive incremental margins.

To further improve service levels, AutoZone plans to double its number of mega-hub stores. These carry over 80,000 SKUs and act as distribution centers to other local stores. Mega hubs supply local stores with same-day inventory and can service many several times a day. When mega hubs open, they noticeably lift sales at all nearby stores.

Beyond commercial, AutoZone continues to increase its store footprint in the US, Mexico, and Brazil. Last year AutoZone opened 138 new stores. It usually opens 200 stores per year, but the pandemic slowed them down this year. We expect them to get back on pace in 2021, which should produce 3% growth on their existing 6,600 store base.

Source: 2020 10-K

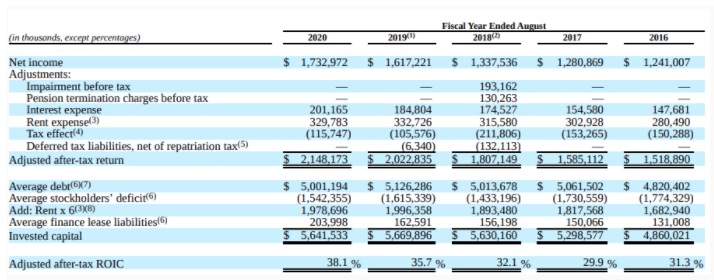

AutoZone’s high incremental returns show up in the financials as a steadily increasing after-tax ROIC. Over the last five years, adjusted after-tax earnings have grown $630 million. Over the same period, invested capital increased by $780 million. The implication is that AutoZone’s $780 million investments produced an 80% return. It worth pointing out that AutoZone can only reinvest about 10% of its earnings at this rate.

The exact number — 80% — isn’t what’s important. What’s important is that it’s high. There are a million ways to slice and dice the financials to estimate incremental returns. Every method points to the fact that incremental returns exceed legacy returns, pushing overall returns higher. Some of what appears to be incremental returns is really operating leverage on existing infrastructure. That doesn’t make the profits any less valuable, though. If comparable sales are flat for a year or two, incremental returns may stagnate. But, in our view, they’re still likely to exceed legacy returns. Over time we expect AutoZone’s ROIC to continue trending higher.

In life and in business you tend to get what you incentivize for. It’s no surprise then that AutoZone incentivizes for high returns on capital. Even better, the vast majority of executive’s pay is “at-risk”.

Source: 2020 Proxy

Compensation at risk is tied to EBIT and ROIC. Not revenues or stock price. We wish more companies aligned incentives so closely between managers and shareholders. If any of our readers have a list of companies that include ROIC in their executive comp plans, please send it our way!

Source: 2020 Proxy

Things are looking up for AutoZone, the business. But what about the stock?

AutoZone’s business return is driven by new store growth and same-store-sales growth. Store count should grow 3% and same-store-sales usually grow 2-3%. Adding these suggest 5-6% annual growth. Another way to think about growth is to multiply AutoZone’s 10% reinvestment rate by the 80% incremental return it generated over the last five years. This suggests 8% annual growth. We wouldn’t count on AutoZone repeating the tremendous run it just had, but we do think 5-6% annual growth possible.

One of our favorite aspects of AutoZone is its “Outsider” capital allocation. AutoZone returns 90% of earnings to shareholders as repurchases. Managers dollar cost average into their own stock, year-in, and year-out. They don’t get cute and try to time the market, they keep it simple. They understand that time in the market is more important than timing the market. Actually, AutoZone did pause its repurchase program in the midst of the March lockdown but subsequently reinitiated the program. The stock’s median P/E multiple over the last 15 years has been 15x, according to Value Line. This implies that repurchases will add about 6% yield, bringing the business’s total return to 11-2%.

AutoZone generated $2.2 billion of free cash flow last year. At $1,150 per share, AutoZone is worth $26 billion and trades for 12x earnings. If AutoZone reverts to it’s 15x multiple in the coming years, the stock will outperform the business and, we expect, produce a satisfactory investment return.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.