Case Study: Pershing Square’s Investment In JCPenny

Today we have a guest post by Nick Corcoran. Nick studies business at The University of Miami of Ohio and serves as President of Markets of the Investment Banking Club. Here is Nick’s LinkedIn page. Please feel free to reach out to him with questions, comments, or opportunities.

If you or anyone you know is interested in working with Eagle Point Capital on a research project like this, please contact us. Our goal is to compile case studies of unsuccessful investments made by otherwise successful investors. In doing so, we hope to learn to avoid situations that lead to a permanent loss. As Charlie Munger says, “All I want to know is where I’m going to die so I never go there.”

Pershing Square Holdings Buys JCPenny

Success is not a straight line up…how successful you are is really a function of how you deal with failure…I’ve always had that view and I’ve certainly had to apply it to myself a few times.

Bill Ackman

Pershing Square Capital, the successful hedge fund led by activist investor Bill Ackman, has had many successes along with a few heavy losses. One of those losses was JC Penney, a soured turnaround. Today we’ll dive into the investment thesis, timeline, and some key takeaways from one of the biggest losses at Pershing Square Capital.

History

Since 1902, J.C. Penny (JCP) has sold family apparel, footwear, jewelry, beauty products, and home furnishings through its network of department stores. Today it operates 850 stores in the US. On May 15th, 2020 it filed for Chapter 11 Restructuring Bankruptcy.

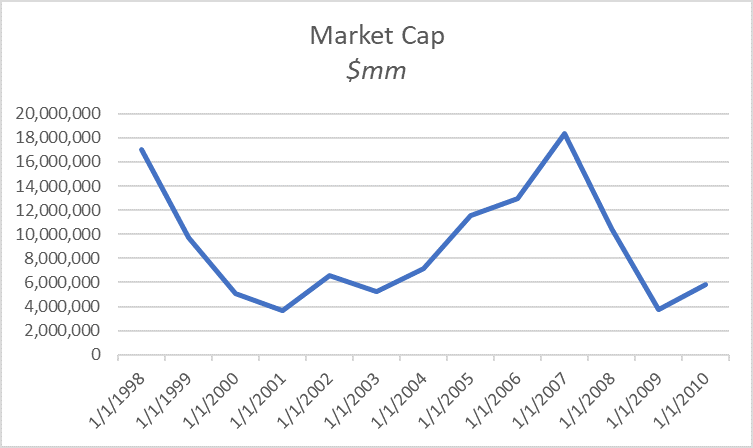

After the death of its founder, JCP has floundered. By 2010 it had fallen from one of the biggest and most successful retailers in North America into a struggling giant failing to keep up with Kohls and Target. The combination of low sales productivity, a bloated expense structure, low margins, and the change to being a discount-oriented brand had caused the company to struggle for the past decade; going from a $17B market cap in 1998 to $3.7B in 2009. Earnings were cyclically depressed, and sentiment was low following the market crash of 2008, which led to a seemingly attractive turnaround opportunity.

JCP Market Capitalization. Source: Data From Yahoo Finance

In 2010 Bill Ackman and Pershing Square disclosed a 39.7mm share position or 16.8% of J.C. Penney’s stock along with “additional economic exposure.” Vornado Realty Trust, a REIT led by Steve Roth and Michael Fascitelli, took a 9.9% ownership position alongside Ackman. Vornado brought their retail and real estate expertise to the table.

Pershing Square’s 2010 Shareholder Letter laid out Ackman’s thesis for the investment, which he also discussed in interviews with the media. Ackman described the potential for significant operational improvements as the key driver to the investment. This meant turning around JCP’s low margins and low sales productivity. 2010’s sales per square foot were at 2002 levels and profit margins were around 1.4%, both flirting with industry lows. The trend they were on was “not survivable” if drastic changes to the business were not made. 2010 adjusted-EBITDA margins were 30% below their 2007 peak, and EBIT margins were also down 45%.

Investment Thesis

Retail businesses come with substantial operating leverage because once the facilities are built there isn’t a lot of excess capital that must be funneled in to operate, beyond labor and inventory. JCP’s 112-year history endowed the company with two advantages. First, a well-recognized brand. Second, low-cost or owned real estate in some of the country’s best malls.

The company had a strong balance sheet with well-laddered debt and non-core assets that could be monetized. Ackman believed he could improve operations, cut unnecessary expenses, monetize non-core assets, and benefit from an improving economy following the great recession.

Ackman wanted to completely change JCP’s business model. He wanted to replace the discounted-merchandise model currently in-place with new revenue streams he could roll-out nationwide. As he had found in past investments, finding a replicable business model with high operational leverage can be extremely profitable and provide significant long-term free cash flows.

Ackman’s Pershing Square was willing to use “time arbitrage” and look longer-term down the horizon than most hedge funds focused on quarterly earnings. Ackman believed that JCP was a “great platform” to build on.

However, JC Penney’s only competitive “moat” as Warren Buffet would put it, was their customer base returning for discounts and coupons, cheap mall retail leases, and their recognition as a great American retailer. Other competitors such as Kohl’s and Target were having more success at the time, stealing customers and improving the shopping experience. Target had created a cost-efficient machine with an expanding customer base, and Kohl’s was a similar public competitor with a profit margin of 6% EOY 2010, far exceeding JC Penney’s margin of 1.43%.

Valuation-wise, 2010’s profit margins were at a cyclical low, ROE was depressed, earnings per share were decreasing. As a result, the stock traded at just a 4.8x PE. This was a company on the decline, but Ackman was prepared to execute a complete turnaround using strategies he had implemented before, like hiring new management and improving operations.

JCP Financial Statistics and Ratios. Source: Data from Yahoo Finance

Management Succession

The only thing Ackman needed was support from the board of directors and a competent CEO. This is where his biggest mistakes were made.

Once Ackman and Vornado joined the board as 2 of 11 seats, they immediately went to work on finding a successor for Mike Ullman, the current CEO. The best name in retail was already someone who the board was investigating and who Ackman was interested in given his history of past successes – Ron Johnson.

As a former senior vice president under Steve Jobs at Apple, Johnson had built the Apple store from scratch. Today Apple stores sport some of the highest sales per square foot of any retailer. Before that Johnson had been Target’s Vice President of Merchandising. Johnson had a reputation as a creative thinker and cost manager. Ackman thought he’d be a perfect fit.

Johnson quit his job at Apple to join JCP. In doing so, he forfeited $100mm of stock options but received $50mm of JCP 7-year options. He personally invested another $50mm in options with a 6-year lock-up. This incredible level of management alignment along with Johnson’s track record set the company up for a turnaround. Ackman had used similar tactics to align Hunter Harrison’s incentives with his at Canadian Pacific to great success.

Backed by the Board, Johnson immediately went to work carrying out Ackman’s strategy – cut expenses, monetize non-core assets, and improve operations. He found $1B in cost savings and monetized $600mm of non-core assets. When Johnson announced his plan to update stores by 2015, the stock soared 24%.

Failures

JC Penney had traditionally marked merchandise at full price and then heavily discounted that price with sales and coupons. Johnson disapproved of this model. He believed the customer understood the merchandise’s value and wanted to follow Apple’s model of fair and full pricing.

He also decided to change the layout of the stores to resemble a more miniature-mall experience with wider lanes and a “town hall” in the center. Here, individual brands could sell while customers got ice cream cones and even haircuts. This would attract an entirely new universe of brands to JC Penney.

However, this led to enormous capital expenditures and a complete overhaul of the business model in a short period of time. Johnson’s model at Apple hadn’t been to test ideas but rather to roll out everything all at once, the opposite of the norm for traditional retail businesses like JC Penney.

Ironically, prior to investing, Ackman had believed one of J.C. Penny’s mistakes was implementing “too much change, too quickly, without adequate testing.” In doing this himself, Johnson destroyed JC Penney’s traditional relationship with its customer. Customers had been conditioned to clip coupons from the Sunday circular and then proceed to the store for markdowns. Without the thrill of markdowns, customers almost immediately stopped visiting the stores.

Meanwhile, Johnson had also fired most of JC Penny’s incumbent executives and replaced them with his own hires. His new COO, Michael Kramer, followed him from Apple. This led to group-think and ultimately created an unhealthy power dynamic.

Ackman was not involved in these decisions, a huge oversight considering how risky they proved. Without a phased rollout to test JCP’s new retailing model, Johnson’s strategy was a bet-the-company shot in the dark. Johnson’s previous success probably led to the hubris of this decision. But all investors know that past success does not guarantee future results. This was a memorable lesson for Pershing Square and its investors.

In Q4 2012, same-store sales plummeted 32%, considered some to be the “worst quarter in retail history.” By February 2nd, 2013, JC Penney had realized $1B in losses. There was no improvement by April so Johnson was fired along with 19,000 employees.

Mike Ullman returned as interim CEO. In August, Ackman wrote to the JCP board about Ullman. He thought he wasn’t making decisions appropriate for an interim position and called for a new appointment in 35-45 days. The board issued a hostile response that expressed their satisfaction with his performance.

Initially, Ackman’s ideas were aligned with the board’s. But, plummeting sales soured the relationship and disagreements over succession ultimately destroyed Ackman’s relationship with the board. In August Ackman resigned from the board and sold all of Pershing Square’s stock, locking in a loss of $500mm. The operating leverage that originally attracted Ackman had gone in the wrong direction, catalyzing the stock’s 57% decline in 2013.

Source: Data From Yahoo

Ackman failed to understand every facet of Johnson’s management style, particularly his inability to accept criticism and learn from failure. Johnson had never made a mistake. Straight out of college, he had met success with success and never had to learn from a substantial setback or failure. This gave Ackman undue confidence and created blind optimism. Confidence led to a lack of risk management, which led to bet-the-company strategic decisions, which ended in failure.

Summary

Bill Ackman’s JC Penney campaign failed due to:

Selecting a CEO ill-suited to JCP’s customers, strategy, and culture;

Blind trust in JCP’s management and poor oversight of their strategy;

Bet-the-company strategic initiatives with little proof of concept;

A failure to connect with and understand the customer.

There are a few lessons to take away:

Not all risk is easily quantified;

Past success does not guarantee future results;

Understanding the customer is paramount; and

Turning around a business with a narrowing moat is likely to be a losing battle.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.