Keep an Eye on CSW Industrials

CSW Industrials is a company of which I would be happy to own 100%. The Dallas-based firm is best classified as an “industrial growth” company and embodies many of the characteristics I look for in a business.

CSW provides specialty solutions for sticky and growing industrial markets, earns attractive returns on capital, and is led by an owner-minded management team with skin in the game.

Overview

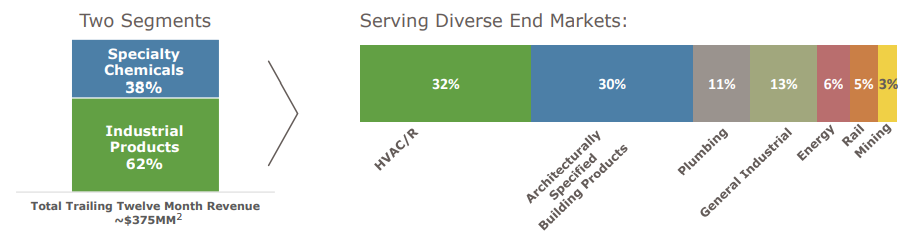

CSW Industrials was spun out of Capital Southwest in late 2015 and operates under two segments; Industrial Products and Specialty Chemicals.

The Industrial Products segment (~60% of revenue) primarily produces mechanical products for HVAC and Refrigeration (HVAC/R) applications and building products for architecturally specified applications. Examples of products include custom-engineered railings and expansion joints, fire-protection products, specialty mechanical products, and storage, filtration and application equipment, among many others.

The Specialty Chemicals segment (~40% of revenue) consists of high performance specialty lubricants and sealants. These products are typically utilized to extend the life of capital equipment such as cranes, rail systems, mining equipment, air conditioning units, water wells and oil rigs.

Across both segments the end market breakdown looks like this:

source: August 2020 Investor Presentation

CSW has a diverse customer base with thousands of end users and no customer representing a material portion of their revenue.

Competitive Position

The terms “industrial products” and “specialty chemicals” often conjure thoughts of extreme cyclicality, commodity exposure, and limited differentiation amongst competitors. Fortunately for CSW, the picture is much brighter.

CSW benefits from several factors across its product portfolio, including:

- They emphasize and compete primarily on superior performance and reliability, where they have an extensive track record, rather than on price;

- Many of their products provide recurring revenue due to the maintenance, repair and consumable nature of their products;

- They sell their products through a vast and engrained distribution network allowing for significant cross-selling and attractive acquisition opportunities;

Value Proposition

Decisions to buy CSW’s products are generally not driven primarily by price. Because many of their products are geared towards asset protection and safety, customers are primarily concerned about performance. Turnover is low among customers given the risks of switching to a competitor compared to the potential savings. The engineers in a glass bottling plant or steel facility generally do not want to risk an expensive piece of equipment breaking down because they skimped on buying the best lubricant. Architects need fire-protection systems that are reliable rather than the absolute lowest price. CSW benefits from this dynamic across its portfolio.

Further, CSW has established themselves as the industry standard in many applications over the last several decades. For example, according to their most recent 10K, their pipe-thread sealant is industry-standard for HVAC/R, and their anti-seize lubricant is recognized as the compound of choice, and requested by name, for oil and gas drilling operations. Owning the industry standard brand in niche markets often means there is little incentive for new entrants, which can be a solid moat. This, combined with their strong relationship with a diverse distribution channel results in CSW often receiving first-look when customers need a new solution. Their exclusive relationship with many distributors also makes it easier to introduce new products and cross-sell with existing customers.

Finally, CSW provides niche and specialty solutions in both segments. The company partners directly with existing customers to come up with application-specific solutions. This inherently limits the potential of large-scale disruption to their business and reinforces customer stickiness.

Once their products are engrained in a customers application, it simply is not worth the hassle and risk to change to a slightly lower cost competitor. These factors have driven organic growth rates ahead of industry averages and solid returns on capital, while also providing an attractive home for acquisition targets, which I’ll discuss later.

Management and Culture

CSW’s management team is consistent and focused when communicating the company’s mission to shareholders. The company emphasizes protecting their employees first, who will in turn take care of their customers and supply chain. They place a heavy emphasis on employee training and report annual training hours (8,500+) to investors. The executive team had a chance to demonstrate their commitment to employees recently by not conducting any furloughs or layoffs due to COVID-19 despite substantial revenue disruptions across portions of their business.

Source: August 2020 Investor Presentation

CEO Joe Armes summed up his attitude towards the business well near the end of their August investor call, saying:

“CSWI has a strong and sustainable business model built upon operating businesses that have decades of history, skilled employees who provide a competitive advantage, an experienced leadership team, a strong balance sheet and a set of core values guiding our actions.

We have deep longstanding relationships with our best-in-class distribution partners. We have a network of proven suppliers and a strong balance sheet…Our commitment to be good stewards of your capital is resolute. To accomplish this goal, we are focused on these four objectives; to treat our employees well, serve our customers well, to manage our supply chains effectively and to position our company for sustainable long-term growth and profitability.”

As Matt detailed last week, we emphasize an ownership mindset in the companies in which we invest, and CSW scores well here. On the August call Armes discussed the company’s ESOP program and highlighted that the program “incentivizes our team members to think like owners”. Insiders own around 7% of the company and more than 50% of the executive teams’ pay is “at-risk” compensation driven by performance, providing aligned incentives with shareholders.

Shown below, 80% of the CEO’s compensation is based on how the business and stock perform rather than an annual salary. Annual bonuses are based off of operating income and operating cash flow metrics, not adjusted EBITDA, revenue growth, or other often irrelevant metrics to shareholders that are so common among public firms. The long-term equity incentives are split fifty-fifty between standard time-based vesting and total stock return against the Russell 2000, a relevant benchmark.

Source: 2020 Proxy Statement

While the incentive plan is not perfect – I’d prefer some measurement of return on invested capital as well - overall the management team says the right things and is incentivized to act like owners, because they are.

Capital Allocation

CSW has a straightforward and sensible capital allocation approach. First and foremost the company vows to maintain a rock solid balance sheet. As of the last quarter CSW held a net cash position with ample liquidity. Next, the management team preaches pursuing the highest risk adjusted return capital allocation decisions, which include investing in organic growth, acquiring new businesses, and returning capital to shareholders via buybacks and dividends.

Source: August Investor Presentation

CSW’s business is not overly capital intensive and does not require hefty capex spending to maintain existing revenues. This results in solid free cash flow available for capital allocation decisions.

Over the years the company has been an active acquirer of businesses that augment their existing product portfolio. The company has acquired more than 30 businesses since 1991 and five since the 2015 spin off. The management team targets “product line” acquisitions with low integration risks that will benefit from CSW’s superior distribution network. During the investor call in August the CEO mentioned that their M&A pipeline remains strong and valuations have not meaningfully increased. I expect them to continue to selectively acquire complimentary product lines for many years.

Growth

CSW has experienced healthy topline growth across almost all segments since the 2015 spin off. Revenue has grown at nearly 10% annually, with 7.2% annual organic growth and 2.5% due to acquisitions. In FY2020, HVAC sales grew 13.7%, plumbing 8.6%, and architecturally engineered products 15%. Smaller markets grew between 1.5 – 9.5%. Management sees this trend continuing as they continue to benefit from strong, though somewhat cyclical, end market demand and the ability to cross-sell new products with existing customers and selectively acquire new product lines.

Over the past five years the business has retained a healthy 65% of operating cash flow for organic and inorganic growth opportunities. They’ve earned around 17% on that incremental invested capital resulting in consistent growth in intrinsic value. Returns on capital have steadily increased since 2015 and it wouldn’t surprise me to see this trend continue as a result of accretive acquisitions, providing additional upside. With a similar reinvestment rate and return on capital going forward, intrinsic value should compound at 10-11% annually.

Turning to shareholder yield, the business initiated a dividend in 2019 and has ramped up share repurchase activity since 2018. The current 0.7% dividend yield is well covered as it represents only ~20% of earnings and I expect management to boost the payout over time. Share repurchases should continue with share count dropping 1-2% annually.

Source: Author, company filings utilizing data from FY2016 – FY2020.

Finally, the business has virtually no debt and therefore has the capacity to undertake larger acquisitions if they find the right opportunity. Using modest leverage for larger acquisitions, ramped up repurchase activity, or special dividends would enhance returns over these base expectations.

For a business like CSW, growth will be slower during an economic downturn, but lower valuations on acquisitions made during recessions, a better buyback yield, and higher growth coming out of recessions seem likely to offset periods of slower growth.

Given the company’s size (only ~$1B market cap), strong end markets, and opportunity to continue to conduct bolt-on acquisitions, I think it’s reasonable for the business to deliver double-digit growth for some time. All told, the business should grow 11-14% per share annually through a cycle before any change in valuation multiple.

Valuation and Forward Returns

Since making its public debut in 2015 CSW has traded at a median 21x earnings and 18x free cash flow (per ValueLine) and currently trades at roughly 24x 2019’s earnings and 18x 2019’s free cash flow. The current valuation seems roughly fair for an above average business with a strong management team, an ample reinvestment runway, and considering the persistently low interest rate environment.

To err on the conservative side, I’ll assume a business per share return of 12% annually (compounding + shareholder yield). Below are returns that I would expect from different purchase price multiples over the course of five years.

Source: Author, company filings

While I think investors do reasonably well from current prices, I plan to watch the business and wait for a pullback before considering buying shares. Because there is some cyclicality in CSW’s end markets, regular volatility in the stock seems probable. Long term investors should be able to find attractive entry points periodically by keeping an eye on the business.

Conclusion

CSW Industrials is an understandable business of which I would be happy to own 100%. With a sustainable business model exposed to sound end markets and a long growth runway, CSW Industrials could grow intrinsic value at a double-digit clip for many years. A strong management team has laid the foundation for what could be a long-term compounding story as they continue to replicate their growth playbook of cross selling an entrenched customer base and periodically acquiring complementary businesses.

Though prospects for the business appear bright, the stock does not represent a “no-brainer” opportunity at the moment given the valuation lacks an adequate margin of safety. I’ll watch CSW closely and given the opportunity to purchase the business at 14 or 15x free cash flow or lower, I would gladly do so as returns could approach high-teens for several years from those levels.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.