NVR And The Housing Cycle

At the risk of stating the obvious, housing is cyclical. Booms lead to oversupply, which leads to lower prices, which leads to a bust. Busts lead to undersupply, which leads to higher prices, which leads to booms. Today we’re at the point where undersupply has led to higher prices, incentivizing builders like NVR to increase supply.

Before the financial crisis, there’d only been two years of housing starts below 1 million units. Since then, there have been six.

Source: Author, Data From The Federal Reserve Bank of St. Louis

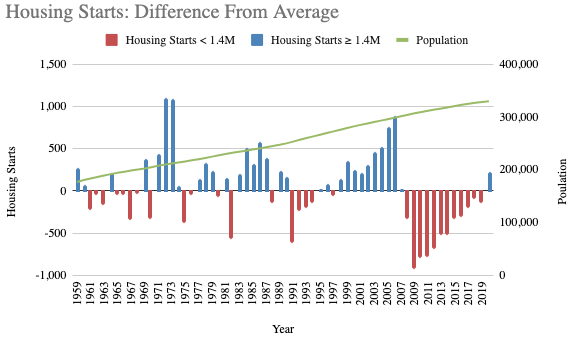

The housing cycle is even more apparent in the next chart. It plots housing starts minus their long-run average of 1.4 million units. 2020 was the first year in twelve that housing starts rose above their long-run average.

Source: Author, Data From The Federal Reserve Bank of St. Louis

The million-dollar question is, did 12 years of under-building more than compensate for the prior ten years of overbuilding? How much excess supply did we need to absorb?

Assuming 1.4 million housing starts is the “right” number that balances supply and demand, the U.S. built 3.8 million extra houses during the 1998-2007 upcycle. Then, the US underbuilt 5.5 million houses during the 2008-2019 bust. Net, the country is missing 1.7 million houses.

This is an imperfect analysis. For starters, the equilibrium number of houses probably isn’t 1.4 million. That’s probably too low. 1.4 million is the long-run average back to 1959. Since then, the population has nearly doubled. Average people per household has also fallen from 3.4 to 2.6. More people plus fewer people per house both point to greater demand for housing.

Although this analysis isn’t precise, it’s probably directionally correct. If it is, the next decade is likely to look a lot better for homebuilders than the last.

Freddie Mac estimated in 2018 that the equilibrium number of new houses is 1.6 million per year. That includes 1.1 million for new household formation, 0.3 to replace old houses, 0.1 for second homes, and 0.1 for vacancy.

Building 1.6 million houses a year would still leave the US 1.7 million in the hole after 12 years of underbuilding. To get back to even over five years, we’d need to build an extra 0.3 million houses through 2025.

If this comes to pass, housing starts will average 1.9 million for the next five years. We’ve only managed this rate of building six times in history, so it would undoubtedly qualify as a boom. But, unlike the last boom, fundamentals, not speculation, would drive it.

To be clear, this isn’t a forecast. I have no idea what housing starts will be next month or next year, let alone in 2025. I only aim to be directionally correct. We probably need to build more houses than we have been building. If we do, homebuilders will do better in the next decade than in the past decade.

There are two more confounding variables to consider. First, real estate is a local market. A buyer in Washington D.C. doesn’t care about the supply of housing in Sacramento. Second, all houses are not created equal. Starter homes and mansions are distinct markets.

Source: Freddie Mac, April 2021

The US population is migrating south. We’ll need to build more houses in the sunbelt than the rust belt. This favors NVR, which primarily builds in the mid-Atlantic region around Washington DC. The chart above shows that this area continues to see a net inflow of migrants. DC anchors the region’s economy and adds stability. This mutes the extremes of the booms and busts seen in places like Miami, Phoenix, and Las Vegas.

Ryan Homes is NVR’s largest subsidiary. It focuses on entry-level starter homes. While the country has been under-building homes in general, underbuilding has been particularly acute for starter homes. According to Freddie Mac, entry-level supply is at a 50-year low.

Source: Freddie Mac, April 2021

As you would expect, this has given NVR a degree of pricing power. In their Q1 10-Q, they wrote:

New Orders were higher in each of our market segments quarter over quarter due to favorable market conditions driven by historically low mortgage interest rates coupled with low resale inventory levels, which drove demand and provided us pricing power.

Pricing power was the cherry on top of a blow-out first quarter. New orders rose 26%, and new order prices rose 10% year-over-year. The value of NVR’s backlog grew by 51%. The table below puts these in their historical context.

Source: Author, Data From SEC Filings

Since 2004, NVR has, on average, increased new orders by 5% and prices by 2%. Although these are relatively small numbers, they’re volatile. 2020’s blow-out results weren’t even the best on record.

Since 2000, NVR’s has compounded earnings per share at 14% annually. This puts it among the best in the S&P 500. 14% is double what increases in volume and pricing would suggest. The difference was due to two other factors.

The first was NVR’s mortgage business. From a standing start, NVR now originates loans for 90% of units NVR sells. NVR maintains a high capture rate by offering buyers discounts on upgrades in return for banking with them. This is a high-margin, capital-light business.

The second was buybacks. NVR’s asset-light model means that it doesn’t need to retain much of its earnings to fund future growth. Historically NVR has required about $150k of equity per unit settled. They can build a house in 100 days, allowing them to turn their capital about 3.5x times per year. As a result, NVR has only retained 7% of its earnings to fund its growth.

NVR used the remaining 93% of earnings to repurchase shares. One of the best things an investor can do is dollar-cost average into a high-ROIC business they understand, like, and admire over many decades. That’s precisely what NVR’s management team has done since the early 1990s. Buybacks have reduced shares outstanding by 4% annually over the last two decades, which has more than halved the share count.

NVR was one of the best-performing stocks of the past twenty years despite facing macro headwinds. We’re eager to see how the company handles a potential boom in the coming years.

We don’t take macro forecasts seriously, even when we make them ourselves. We don’t try to predict cycles. Instead, we prepare. NVR’s unique capital-light business model ensures the company won’t get caught with excess inventory at a market top. It was the only public builder to earn a profit through the 2008 downturn. Though its earnings are cyclical, they’re unlikely to go negative.

Source: Author, Data From 10-Ks

Knowing NVR’s balance sheet is clean and conservative helps us sleep at night. We don’t need to forecast housing starts to do well with NVR. But, if we’re directionally correct, the next decade should be even better than the last.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.